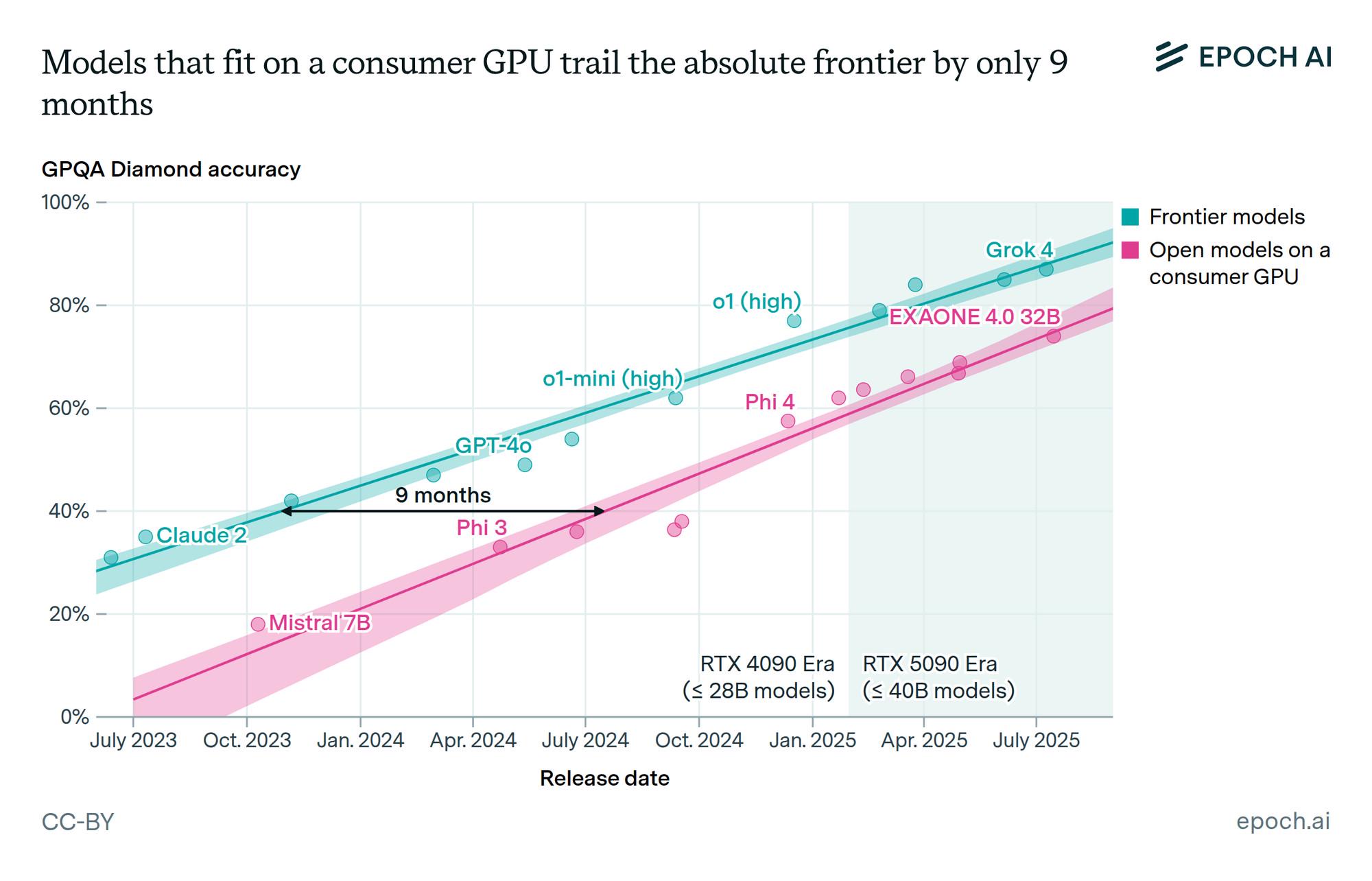

The Shifting Landscape of AI: The Rise of China¶

On September 30, 2025, something unremarkable happened: a Chinese AI company called Z.ai released GLM-4.6, a new large language model. The release came one day after Anthropic shipped Claude Sonnet 4.5, roughly seven weeks after OpenAI launched GPT-5. Three frontier models in two months. Just another week in AI.

Except it wasn’t.

What made GLM-4.6 significant wasn’t its performance, though it achieves near-parity with Claude Sonnet 4 (48.6% win rate). It wasn’t even that it trails Claude Sonnet 4.5 in coding, currently the benchmark. What mattered was the price tag.

GLM-4.6 costs $0.50 per million input tokens and $1.75 per million output tokens. Claude Sonnet 4.5? $3 input, $15 output. That’s 6-8.5 times cheaper for roughly comparable performance. Put another way: developers paying $200/month for Claude Max can get similar coding assistance through GLM for $3-15/month.

GLM-4.6 costs $0.50 per million input tokens and $1.75 per million output tokens. Claude Sonnet 4.5? $3 input, $15 output. That’s 6-8.5 times cheaper for roughly comparable performance. Put another way: developers paying $200/month for Claude Max can get similar coding assistance through GLM for $3-15/month.

This is the kind of price disruption that doesn’t just change markets. It restructures them.

The commoditization playbook¶

There’s a predictable pattern to technology disruption. A dominant player charges premium prices justified by superior performance. Then a competitor arrives offering “good enough” performance at a fraction of the cost. The premium player insists quality matters. For a while, it does. Then the “good enough” competitor improves. The performance gap narrows. The price gap remains. Premium positions erode.

We’ve seen this play out in cloud computing, smartphones, and solar panels. Now watch it unfold in AI.

The twist? This time the disruption isn’t coming from scrappy startups in garages. It’s coming from a coordinated ecosystem backed by the world’s second-largest economy, one that has decided technological self-sufficiency isn’t optional.

DeepSeek and the efficiency revolution¶

Remember January 2025? DeepSeek announced it had trained a frontier reasoning model for approximately $294,000 (plus $6 million for the base model), not the hundreds of millions Western labs were spending. Silicon Valley’s response oscillated between skepticism and panic.

Remember January 2025? DeepSeek announced it had trained a frontier reasoning model for approximately $294,000 (plus $6 million for the base model), not the hundreds of millions Western labs were spending. Silicon Valley’s response oscillated between skepticism and panic.

The skeptics were wrong. Chinese AI makers have learned to build powerful models that perform near the most advanced U.S. competition while using far less money, chips, and power.

Here’s what matters: DeepSeek isn’t alone. China now has a mature AI ecosystem: GLM, Alibaba’s Qwen, Moonshot AI’s Kimi, Baidu’s Ernie. Each independently capable of frontier research. Each pushing efficiency as hard as capability.

U.S. export controls, intended to slow China’s AI development by restricting access to advanced chips, may have achieved the opposite. Constraints forced innovation. When you can’t outspend your competition, you have to outsmart them. China’s AI labs, working with inferior hardware, learned to extract more from less.

That knowledge doesn’t disappear when better chips become available.

The September surprise (!)¶

Then came September’s watershed moment. China’s Cyberspace Administration banned domestic tech companies from buying Nvidia AI chips. Not as retaliation. As confidence. Beijing concluded that domestic alternatives from Huawei, Cambricon, Alibaba, and Baidu now match Nvidia’s China-specific products.

The speed of adaptation was striking. DeepSeek’s V3.2-Exp model launched with same-day optimizations for Huawei’s Ascend hardware. Not as an afterthought. As a first-class platform.

The speed of adaptation was striking. DeepSeek’s V3.2-Exp model launched with same-day optimizations for Huawei’s Ascend hardware. Not as an afterthought. As a first-class platform.

For Nvidia, this is existential. CEO Jensen Huang acknowledged the disappointment and revealed the company has told analysts to exclude China from forecasts. That’s not spin. That’s a company recognizing it just lost its largest market while that market simultaneously became self-sufficient.

The strategic implications extend beyond Nvidia. U.S. chip restrictions were the cornerstone of America’s plan to maintain AI leadership. If China can build competitive AI systems without American chips, that strategy just collapsed.

Will western developers actually switch to chinese models?

Will western developers actually switch to chinese models?

The standard objections sound compelling: data sovereignty, surveillance concerns, potential backdoors in generated code. For government agencies and defense contractors, these concerns rightly preclude adoption.

But for the rest of the market? History isn’t encouraging for the premium providers.

Developers are ruthlessly pragmatic. They use what works and what they can afford. Right now, GLM offers Claude-level performance at 97% lower cost. For startups burning through runway, for solo developers building side projects, for teams in price-sensitive markets, that’s not a minor consideration. It’s determinative.

The parallel to cloud computing is instructive. When AWS launched, enterprises worried about data security and vendor lock-in. Many still moved to the cloud. Performance and economics overwhelmed abstract concerns. The same dynamic is playing out now, just faster.

And here’s the uncomfortable truth: similar worries about U.S. companies storing user data rarely prevented adoption of American platforms. Users consistently prioritize performance and cost over privacy concerns, until something forces their hand.

The only potentially preventing hindering factor for a massive adoption of Chinese AI technologies is plain xenophobia.

Some silver-lining: Europe’s narrow window

This creates an unexpected opening for Europe.

Mistral AI and similar European efforts have positioned themselves as the third way: neither American surveillance capitalism nor Chinese state oversight. Privacy by design, not afterthought. Openness without geopolitical strings attached.

It’s a compelling pitch. The execution remains uncertain.

European models don’t yet match frontier performance. European companies lack the capital of their American rivals and the state backing of their Chinese competitors. But as U.S.-China competition intensifies, as users grow uneasy with both alternatives, that positioning could matter.

The window is narrow. The question is whether European companies can scale before it closes.

Next¶

OpenAI and Anthropic won’t disappear. They’re too capable, too well-funded, too embedded in enterprise infrastructure. But their business models assume they can charge premium prices indefinitely.

Can they? When competitors offer 80-90% of the performance at 10-15% of the cost?

The pattern is familiar. Premium positions feel permanent until suddenly they’re not. Markets commoditize. Value migrates. The question isn’t whether this happens in AI. It’s how fast, and what these companies do about it.

China’s approach, combining open-source models, competitive performance, and radical cost advantages, isn’t a temporary arbitrage. It’s a sustainable strategy. As long as Chinese labs can access talent (they can), computing resources (increasingly domestic), and global research (through open-source contributions), they can maintain this advantage.

The West’s response options are limited. You can’t out-subsidize China’s state backing. You can’t impose chip restrictions that are already obsolete. You can compete on innovation, but China is innovating too, and under greater constraints.

The assumption underpinning Western AI strategy, that technical leadership translates to market dominance, is being tested. What happens when technical leadership becomes “good enough” and cost leadership becomes decisive?

We’re about to find out. The restructuring isn’t coming. It’s already here and the only question is how long it takes the market to notice.